Profit Margin Tops Forecasts, Reinforcing Bullish Valuation Narratives")

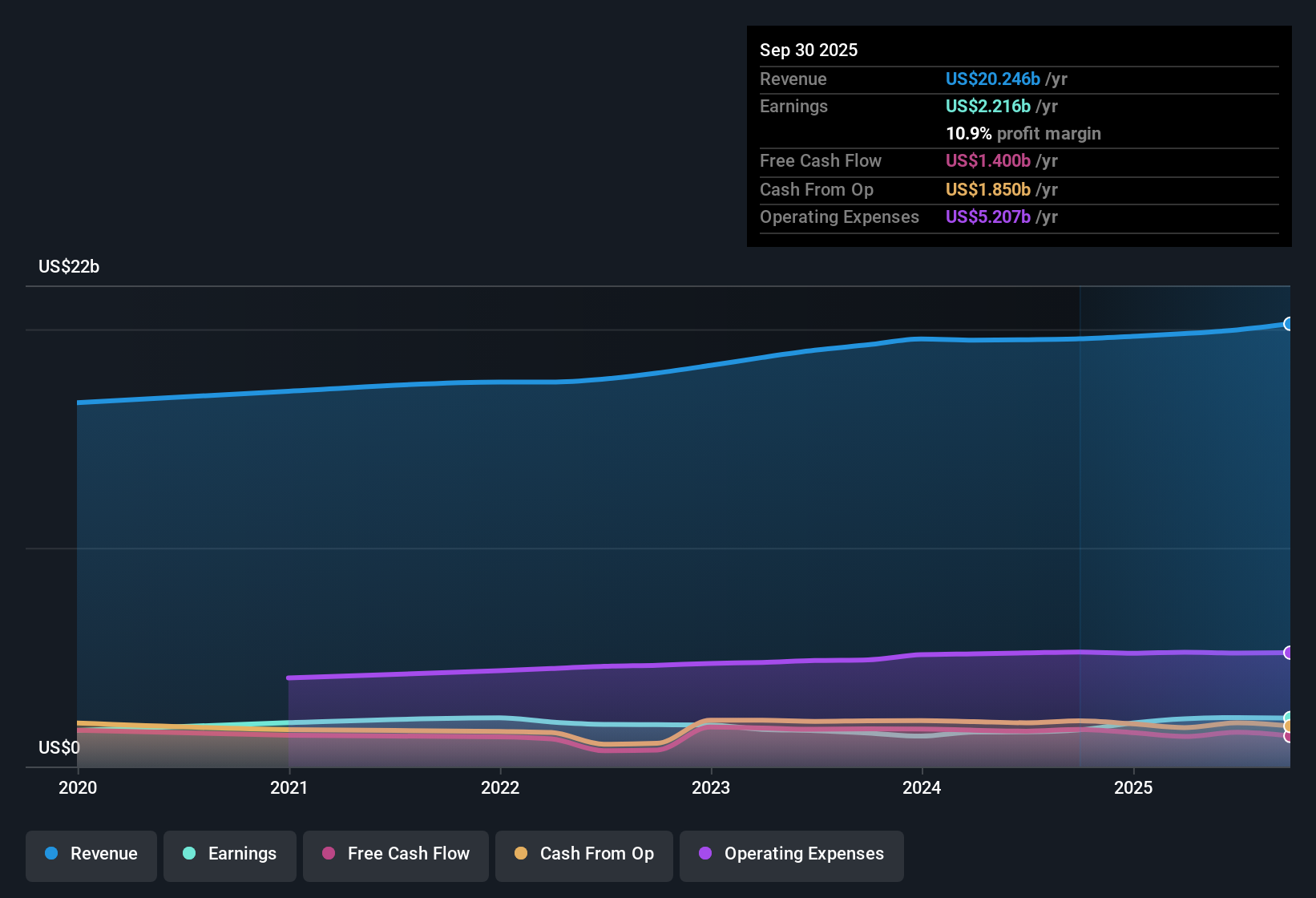

GE HealthCare Technologies (GEHC) delivered a net profit margin of 10.9%, up from 8.6% a year ago, as annual earnings growth surged to 32.3%, far outpacing its five-year average rate of 0.06%. Looking ahead, earnings are projected to grow at 5.6% per year, while revenue is expected to rise at 4.1% per year. Both rates trail the broader US market averages. The combination of expanding margins and favorable value multiples is giving investors plenty to consider this earnings season.

See our full analysis for GE HealthCare Technologies.

Next, these fresh results will be compared with the narratives circulating among analysts and the investment community to see if the numbers support or challenge the prevailing stories.

See what the community is saying about GE HealthCare Technologies

DCF Fair Value Far Exceeds Share Price

- GE HealthCare’s current share price of $75.00 is trading at a substantial discount to its DCF fair value estimate of $128.30. This presents a potential upside of over 70% if this valuation holds.

- According to the analysts’ consensus view, this discount reflects several factors:

- The consensus target price is $88.44, which is 18% below the DCF fair value and 18% above today’s price. This signals that analysts see reasonable upside, though not all agree, as targets range from $73.00 to $106.00.

- To align with consensus, investors would need conviction in projected 2028 revenues of $22.7 billion, $2.5 billion in earnings, and a forward PE of 20.2x. These assumptions are open to debate depending on expectations for the health tech industry’s growth and margin resilience.

- The consensus narrative highlights that the current pricing gap may not close if concerns about tariffs and regulatory risks intensify. Investors should pay close attention to this balance between valuation multiples and macro risks.

What do analysts really think GE HealthCare is worth, and how do the numbers behind this consensus narrative stack up to the latest market reaction? 📊 Read the full GE HealthCare Technologies Consensus Narrative.

Profit Margins Outpace Industry Norms

- GE HealthCare achieved a net profit margin of 10.9%, outpacing its five-year average of just 0.06% annual earnings growth and surpassing the previous year’s 8.6% margin. This margin places it comfortably above most medical equipment peers by profitability measures.

- The consensus narrative underscores the company’s push to broaden its recurring revenue base:

- Growth in digital solutions and high-impact diagnostics are highlighted as drivers that could further stabilize and elevate margins, with pipeline launches like Radiopharmaceuticals and Photon Counting CT expected to help future proof earnings power.

- This dynamic supports analysts’ relatively optimistic earnings growth outlook of 5.6% per year. However, both revenue and earnings forecasts remain below the broader US market average, raising questions about the sustainability of this profitability edge over industry cycles.

Peer Valuation Gap Stands Out

- The company’s price-to-earnings ratio of 15.5x is significantly lower than both the US Medical Equipment industry average (28.0x) and peer group average (36.1x). This signals a notable valuation gap that could be appealing for value-focused investors.

- The consensus narrative notes this discount may be justified by perceived risks:

- Ongoing China trade tensions and potential regulatory changes are highlighted as factors that could limit financial flexibility or impede market share gains going forward.

- Despite analyst optimism on margin expansion and new product launches, consensus remains split about whether GE HealthCare’s lower valuation reflects market caution on near-term risks rather than fundamental weakness in its business model.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for GE HealthCare Technologies on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Have your own take on these figures? It only takes a few minutes to shape your perspective into a narrative that could influence how others view GE HealthCare. Do it your way

A great starting point for your GE HealthCare Technologies research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

While GE HealthCare delivers promising margin expansion, its projected revenue and earnings growth lag the wider market. This casts doubt on its ability to sustain this edge.

If you prefer companies showing steadier momentum, check out stable growth stocks screener (2094 results) to discover stocks consistently expanding revenues and profits, built to weather market cycles with more predictability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link